Debt relief programs are rapidly increasing in popularity. When creditors are breathing down your back, you need someone to help you take care of the problem. However, you want to make sure that you actually owe those debts before you pay them. This is when the process of Debt Validation becomes extremely important. Debt validation, in simple terms, is the process where a debt collector proves that you owe the debt they are trying to collect.

When a creditor is unable to collect the money owed to them, they will usually hire a collection agency to collect the money for them. Often, the debt is actually sold to agencies and is considered “junk debt.” Junk debt is purchased by third parties for pennies on the dollar. These collectors often do not have the correct documentation to prove that the debt is really owed. This is why debt validation is important.

If these collection agencies cannot prove that you owe the debt, then you don't have to pay it. You may have already paid off the debt, but the orriginal creditor did not notify the collection agency. Other times, the orriginal creditor has simply charged the debt off.

To complete a validation, you must ask a debt collector for proof of debt. This is done after a collector informs you of the debt. You have 30 days to request proof of the debt or the collection agency will assume that it is valid and continue in their collection efforts. However, you can request a validation of the debt at any time. This process is designed to keep honesty in the debt collection industry.

Before you pay a debt that you are unsure of, complete the debt validation proccess. If the collection agency cannot provide proof that the debt is yours, you will not have to pay it!

The proccess of Debt Validation is simple, and you can definitely do it yourself. Use our FREE GUIDE to DIY Debt Validation by clicking on the link below, and get started today!

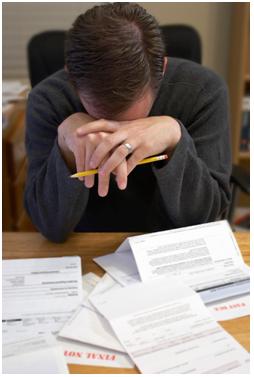

Here you are again. You just deposited your pay check and it is time to pay the bills. As always, you are just barely getting by. You are juggling your bills, your due dates, and your grace periods each and every month. You have so many balls in the air, you can't keep them straight. Sooner or later, one of the balls will drop and your financial "plan" will come toppling down.

Here you are again. You just deposited your pay check and it is time to pay the bills. As always, you are just barely getting by. You are juggling your bills, your due dates, and your grace periods each and every month. You have so many balls in the air, you can't keep them straight. Sooner or later, one of the balls will drop and your financial "plan" will come toppling down.

There is nothing more stressful than being in debt. Every morning people in debt wake up and think about what they can do, and they go to sleep at night worrying about it as well. They aren't alone. According to the Washington State Department of Financial Institutions, 40 percent of American families live beyond their means and the average household with debt has about $10,000 to $12,000 in revolving debt and about nine credit cards. Getting out of debt can be very difficult, especially if people are putting all their income toward paying off the interest alone. But stressing about debt doesn't help; action does. Here are three steps that will help you learn how to cope with financial stress.

There is nothing more stressful than being in debt. Every morning people in debt wake up and think about what they can do, and they go to sleep at night worrying about it as well. They aren't alone. According to the Washington State Department of Financial Institutions, 40 percent of American families live beyond their means and the average household with debt has about $10,000 to $12,000 in revolving debt and about nine credit cards. Getting out of debt can be very difficult, especially if people are putting all their income toward paying off the interest alone. But stressing about debt doesn't help; action does. Here are three steps that will help you learn how to cope with financial stress.  Debt Settlement vs. Bankruptcy?

Debt Settlement vs. Bankruptcy? In order to pay off credit card debt successfully, it is important to commit yourself to improving your financial situation for the long term. There is no such this as a quick fix. Getting out of debt takes dedication and a realistic plan. With so many options to choose from, it can be overwhelming to figure out where to begin, where to seek advice, and whether you should tackle the debt on your own or enlist the services of a debt relief provider. Let's look at your options.

In order to pay off credit card debt successfully, it is important to commit yourself to improving your financial situation for the long term. There is no such this as a quick fix. Getting out of debt takes dedication and a realistic plan. With so many options to choose from, it can be overwhelming to figure out where to begin, where to seek advice, and whether you should tackle the debt on your own or enlist the services of a debt relief provider. Let's look at your options.

times of our history.

times of our history.

If I just make the minimum payments due on my credit cards, will I ever pay them off?

If I just make the minimum payments due on my credit cards, will I ever pay them off?