Do you find it difficult to manage multiple debt payments and due dates each month? If you don't stay organized you can easily pay your bills late and that can add up to hundreds of dollars in late and over limit fees.

Do you find it difficult to manage multiple debt payments and due dates each month? If you don't stay organized you can easily pay your bills late and that can add up to hundreds of dollars in late and over limit fees.

One way to help with this problem is to combine your debt into one low interest Debt Consolidation Loan.

5 Benefits to Debt Consolidation Loans

#1 Consolidate Your Debts Into One Monthly Payment: Using debt consolidation loans, you can pay off all or most of your unsecured bills (credit cards, payday loans, medical bills etc) at once. You're then left with a single loan, which you'll repay through an affordable payment plan.

#2 Eliminate collection calls: You can use your Debt Consolidation Loan to pay off debts that are past due or in collections. This will eliminate harrassing calls and letters from your creditors and collection agencies.

#3 Reduce Your Interest Rate: Debt Consolidation Loans are often offered at lower rates than credit cards. By combining your high interest credit debt into a low interest Debt Consolidation Loan, you will reduce your monthly payment and save money.

#4 Easier Monthly Budgeting: A Debt Consolidation Loan offers a monthly payment that stays the same over the course of the loan. This one consistent monthly payment makes monthly budgeting much easier. Create your household budget using this FREE BUDGET WORKSHEET.

#5 Improve Your Credit Score: When you pay off multiple debts with a single Debt Consolidation loan, and making consistent monthly payments, your credit score will improve quickly.

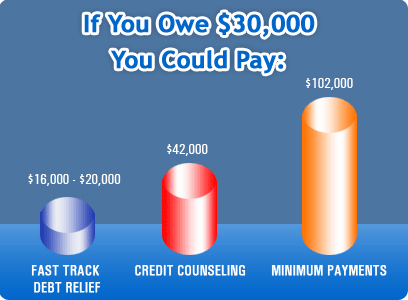

It can be difficult to qualify for a Debt Consolidation loan. If you are not able to qualify for a Debt Consolidation loan, you may want to consider enrolling in a Debt Consolidation Program instead. These programs combine your monthly debt payments into one lower payment while reducing your interest rate and eliminating your debt in just 3-5 years!

For more information on Debt Consolidation and other Debt Elimination programs, please give us a call or simply click on the link below for a FREE DEBT ELIMINATION SUMMARY!

Welcome to 2012! It is a new year, and most people are thinking about a total body makeover. That's right, it's time to start that diet and get back to the gym. But I bet your finances could use a makeover too. Now is a great time to take a close look at your financial situation, set some goals, and make positive changes to help you achieve financial fitness in the New Year!

Welcome to 2012! It is a new year, and most people are thinking about a total body makeover. That's right, it's time to start that diet and get back to the gym. But I bet your finances could use a makeover too. Now is a great time to take a close look at your financial situation, set some goals, and make positive changes to help you achieve financial fitness in the New Year! If you’re struggling with debt, you likely feel like the weight of the world is resting on your shoulders each and every day. Whether it is due to student loans, mortgages, credit cards or other financial struggles, the clutches of debt are enough to make anyone feel trapped and helpless. Luckily, no matter how bad your debt may seem, there are techniques for living debt free.

If you’re struggling with debt, you likely feel like the weight of the world is resting on your shoulders each and every day. Whether it is due to student loans, mortgages, credit cards or other financial struggles, the clutches of debt are enough to make anyone feel trapped and helpless. Luckily, no matter how bad your debt may seem, there are techniques for living debt free.

The holiday season seems to be a season of excess. Eating too much pie or drinking too much eggnog is one thing. Charging too many gifts on your credit cards is another.

The holiday season seems to be a season of excess. Eating too much pie or drinking too much eggnog is one thing. Charging too many gifts on your credit cards is another. Got Wedding Debt?

Got Wedding Debt?

School's Out For the Summer!

School's Out For the Summer!

Are you trying to get out of debt but having trouble paying down your credit card bills?

Are you trying to get out of debt but having trouble paying down your credit card bills? So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

Create a Plan to Pay Off Your Debt

Create a Plan to Pay Off Your Debt