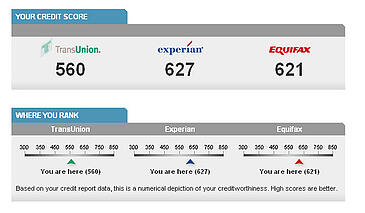

You want a good, clean credit report, right? Of course you do. We all want to keep our credit as tidy so we can borrow money at a low interest rate and keep our insurance rates and security deposits down. It is very important to work on raising your credit score, but it is also important that you understand what does not affect your score. That way you won’t spend time worrying about things that just don’t matter.

Here are 6 things that can’t hurt (or help) your credit scores:

#1: Your Personal Information

Personal information such as your name, current and previous addresses, Social Security number, and birth date is included on your credit report with each of the three main credit reporting bureaus. However, this information does not have any bearing on your credit score. They also cannot factor in your age, education level, race, gender or marital status.

#2: Income Changes

Most people are surprised to learn that income isn’t included on your credit report. As long as you continue to pay your bills on time, earning less has no negative effect on your credit scores. However, creditors generally ask for your income information on their applications. So, making less money could be a stumbling block to getting new credit because in addition to your credit score, your income, expenses, and job stability are taken into consideration by a lender.

#3: Getting Turned Down for Credit

Although your credit report does show who has been looking at your credit report, your credit report doesn’t show whether an application for a loan or credit card was approved or declined. Don’t worry if you’ve been turned down for credit. This has absolutely no effect on your credit score

#4: Paying Small or Local Companies

Bills you pay to small companies or individuals for local services like lawn care, pest control, or rent, usually don’t show up on your credit report. The main credit bureaus have strict requirements about who can report consumer information to them, and in many cases it’s just not feasible for small businesses to do so.

If a merchant doesn’t report payment information to the credit bureaus, then your payment history with that company can’t affect your credit scores. However, if you don’t pay up and they turn your account over to a collection agency, that’s another story! Collection companies will report information to the credit bureaus as soon as they acquire the debt.

#5: Adding an Authorized User

Adding someone to your credit card as an authorized user allows them to get a card in their name and to make charges up to the credit limit that you allow. An authorized user has no legal responsibility to repay the debt. Their credit situation can’t affect yours in any way.

However, your credit scores could plummet if an authorized user abuses a credit card and you can’t afford to make the minimum monthly payments. So always be cautious about adding anyone to your credit cards.

#6: Checking Your Own Credit

Many people worry about pulling their credit report because they think that it will count against them. Pulling your own credit report is called a “soft pull” and it does not hurt your credit scores.

Understanding what does and does not have an effect on your credit score will help you to focus your efforts in the right areas. If you need help eliminating debt once and for all, our Debt Solutions Specialist can explain what programs are available to help you no matter what the situation. Simply give us a call or click on the link for a free debt elimination consultation.

photo by: Casey Serin

When most people think of a credit check, they think of this vague thing where the someone checking their credit puts in their name and other private information and gets this number along with everything they have ever done wrong financially. However, it’s a little known fact that there are actually two kinds of credit checks: Hard Pulls and Soft Pulls.

When most people think of a credit check, they think of this vague thing where the someone checking their credit puts in their name and other private information and gets this number along with everything they have ever done wrong financially. However, it’s a little known fact that there are actually two kinds of credit checks: Hard Pulls and Soft Pulls.